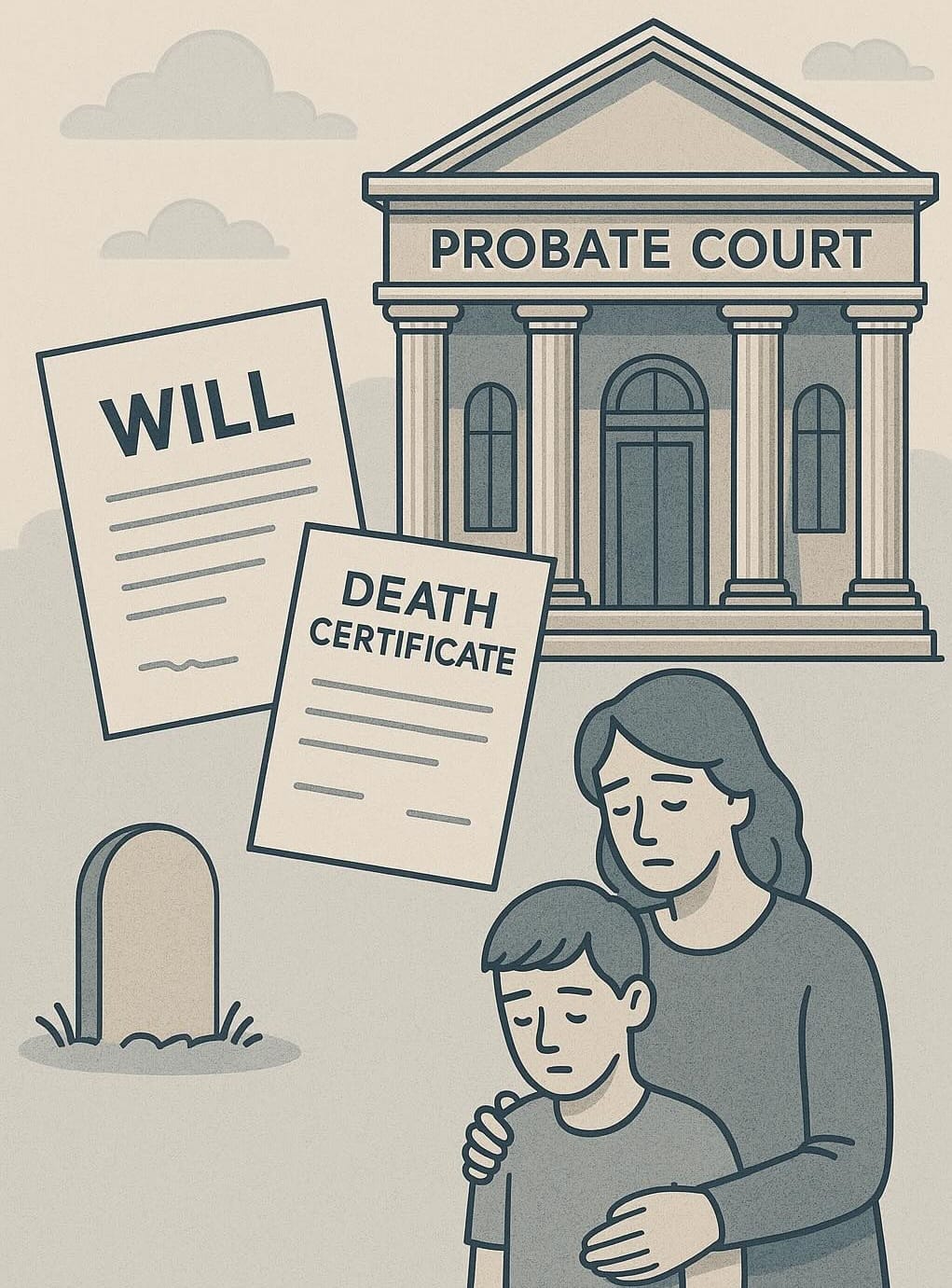

By Raghuveer Surisetty in With Free Subscription : 3 Min Read — 23 Aug 2025 Will, Trust and Probate - Probate and Non Probate Assets

open to all: 3 min read 2-Step Fixed Indexed Annuity Strategy for Secure Retirement In this article, we will see how someone can take a portion

With Free Subscription : 3 Min Read Term Life Insurance from Employer: Gaps and Considerations The life insurance provided by an employer is called group life insurance.

with free subscription : 1 min read Term Life Insurance Across Borders: Comparing Cost in India and the USA In this article we compare the cost of term life insurance in

with free subscription : 2 min read Term Life Insurance: Cost, Riders, and Living Benefits You Should Know