By Raghuveer Surisetty in with free subscription : 2 min read — 26 Apr 2025 How Fixed Indexed Annuities Work: A Visual Breakdown

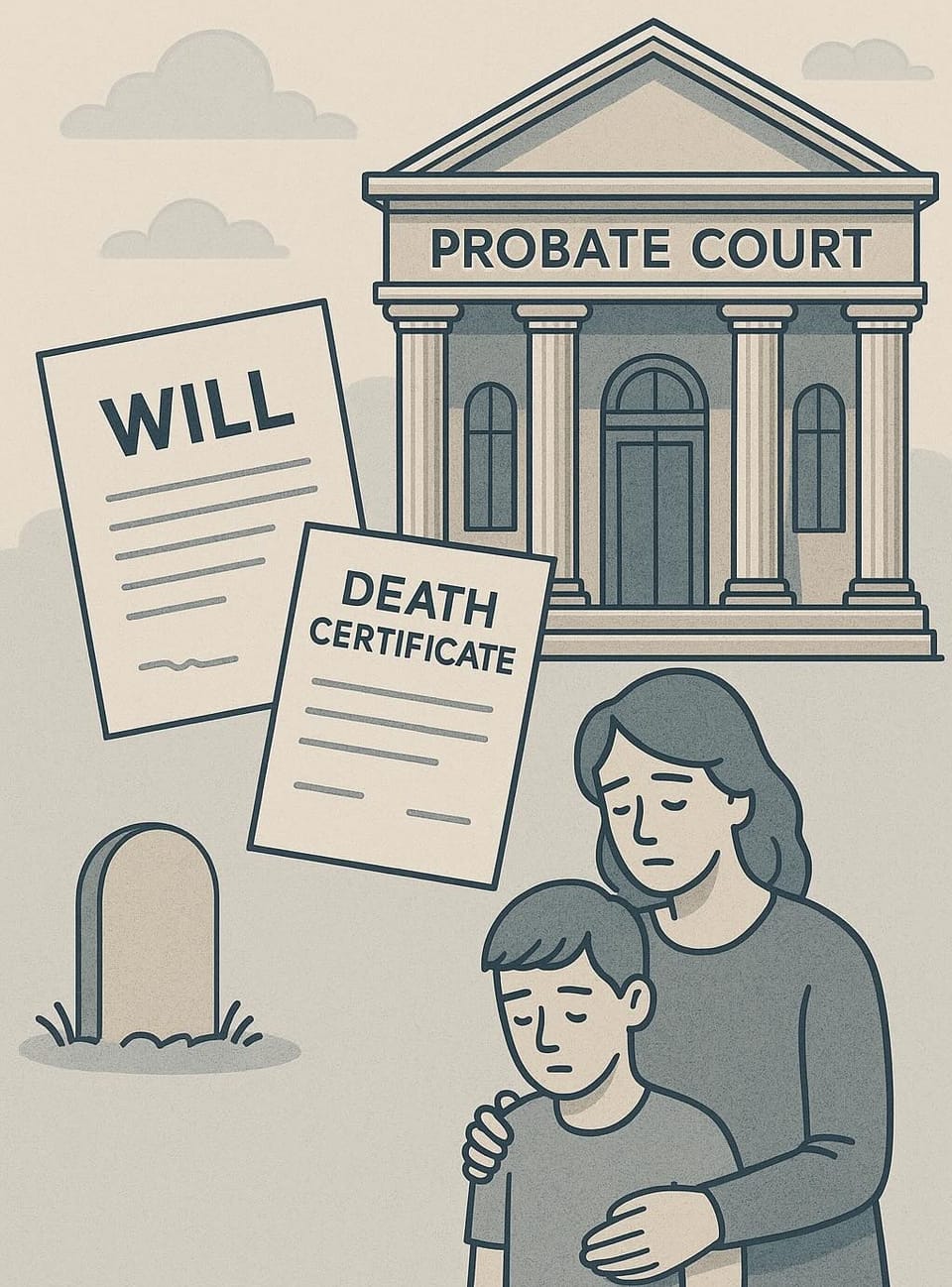

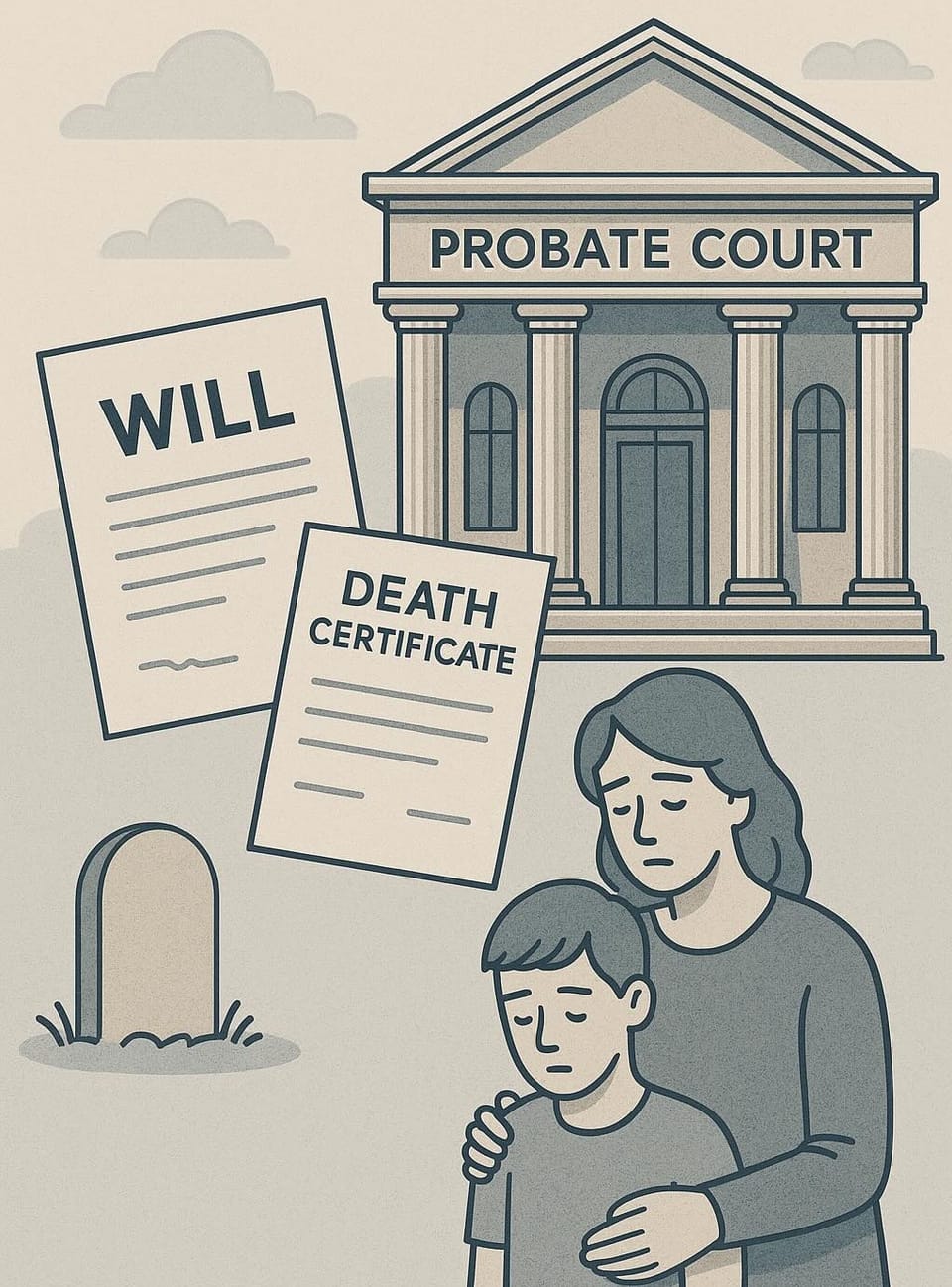

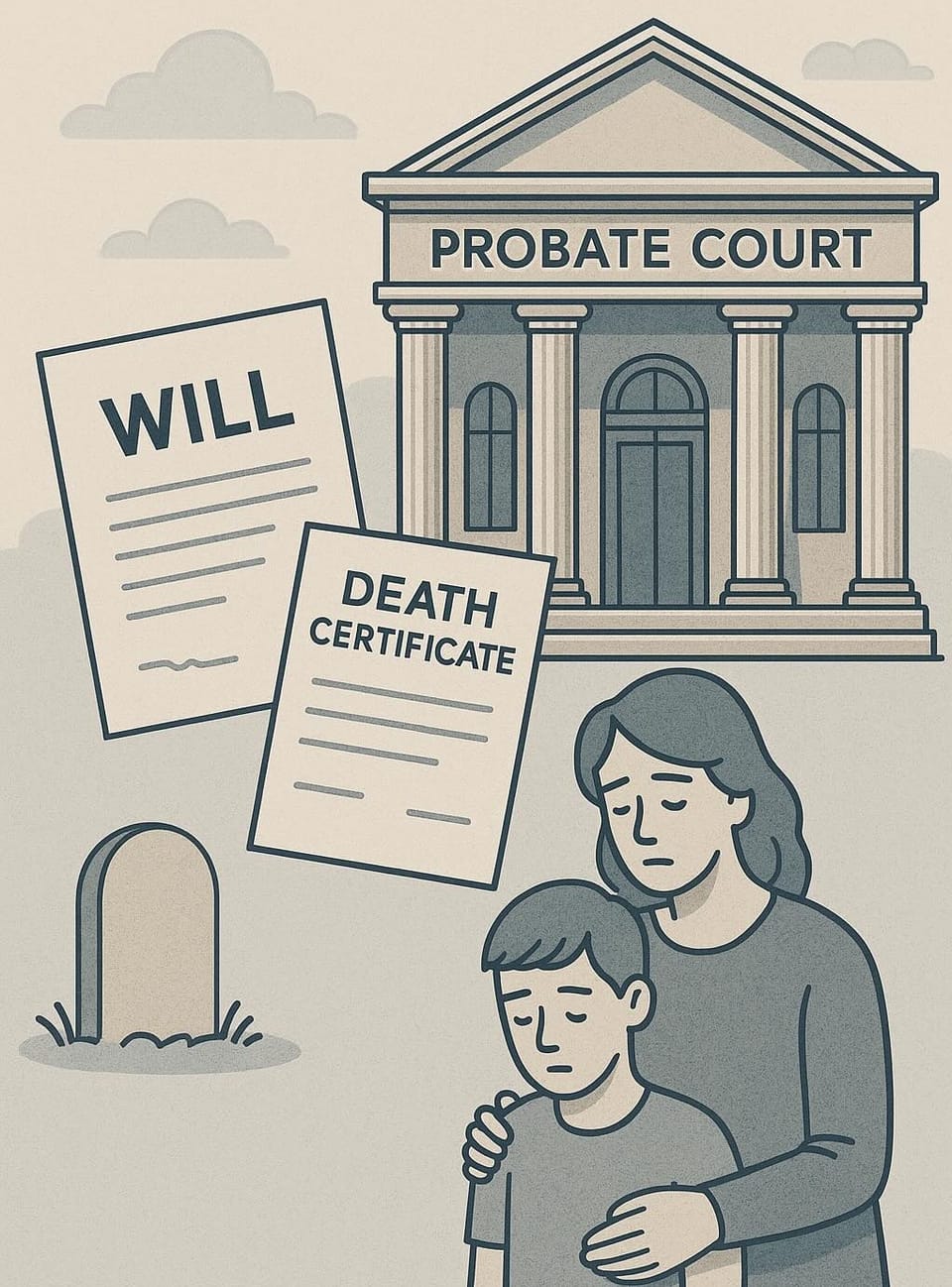

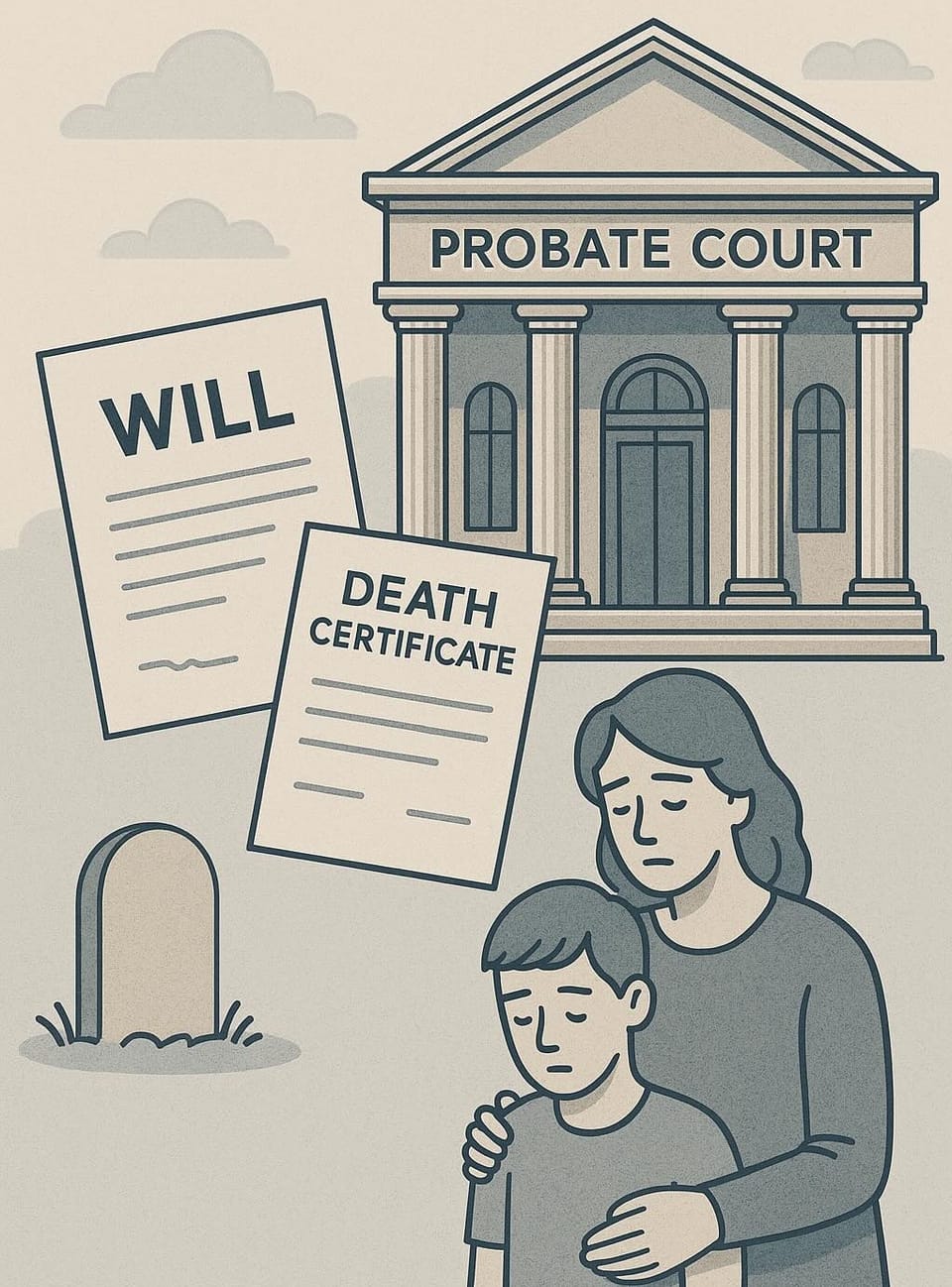

with free subscription : 2 min read Revocable Living Trust With Pour-Over Will We have discussed quite a few topics on wills and trusts. By